Blog

What 300+ conversations taught me over the last year

Feb 1, 2026

I want to start this month with a bit of context.

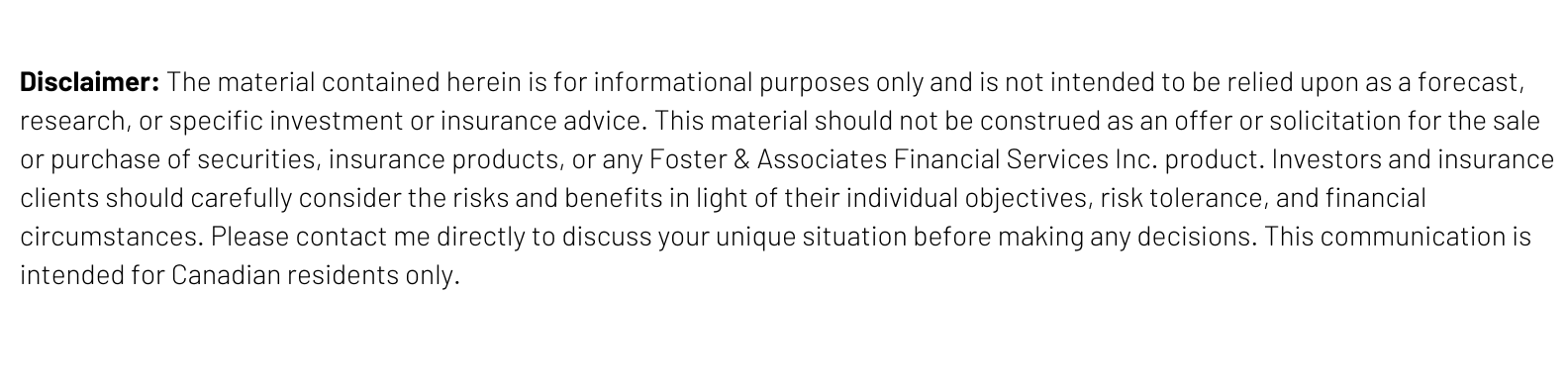

Over the last 90 days, 90 people booked calls with me.

Most were 15 minute intro calls, some turned into full planning conversations, and many were people who had never spoken to a financial advisor before.

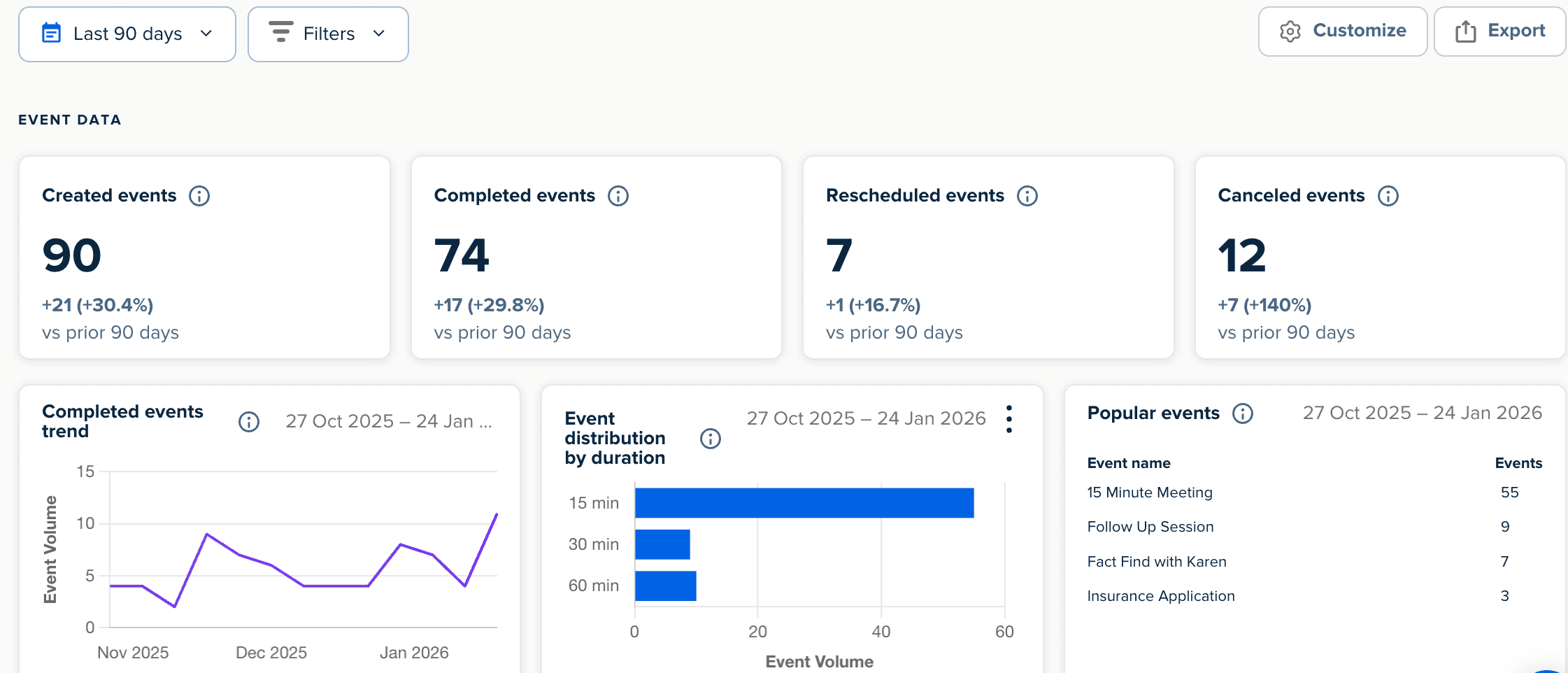

Zooming out, over the last year I’ve had more than 300 intro and planning calls scheduled.

I’m not sharing that to boast. I’m sharing it because it means I’m exposed to a huge volume of questions about money, life, work, stress, confidence, and decision-making. When you hear the same questions repeatedly, patterns start to show up.

And one of the biggest patterns is this:

The people asking the best questions are usually already doing far better than they give themselves credit for.

Which brings me to something I’ve been thinking about a lot lately.

Permission without pretending

There’s a concept in marketing that says people don’t always buy function. Sometimes they buy permission.

Permission to see themselves differently.

Permission to act differently.

Permission to step into an identity before they feel ready.

In the financial world, I see this constantly.

People think confidence comes after everything is figured out.

In reality, confidence usually comes from acting like someone who takes responsibility, asks better questions, and makes decisions before things feel perfect.

You don’t wake up one day and suddenly become “good with money.” You start behaving like someone who respects their future self, even when things feel overwhelming.

Traits I see in people who do really well

I work with people across many incomes, industries, and family situations. What separates the ones who build real stability and wealth over time is rarely intelligence or luck.

It’s usually some combination of these:

They ask thoughtful questions instead of avoiding uncomfortable ones

They take action before feeling 100% certain

They’re willing to look at their numbers

They understand that consistency beats intensity

They invest in their health, skills, and relationships alongside their finances

Most people drift. The people reading this probably don’t.

If you read newsletters like this, book intro calls, or want to understand the “why” behind your decisions, you’re already behaving like someone in a very small slice of the population.

You don’t need to be perfect. You just need to be consistently not careless in areas where most people are.

That alone puts you far ahead.

Some of the common questions I hear every week

“I’m doing okay, but I don’t feel secure. Is that normal?”

Very normal. Most people are juggling careers, family, health, and life admin. Money often gets pushed aside until it creates anxiety.

Clarity helps. Knowing how much you should be setting aside, at your age, to retire comfortably removes a lot of stress.

“Am I behind for my age, or does it just feel that way?”

Almost everyone I speak to between 35 and early 50s feels behind. Every single one.

Timelines matter, but with the right structure and a realistic plan, most people get far closer to their goals than they expect. Feeling behind usually means you haven’t seen the full picture yet.

“Should I focus on my TFSA, RRSP, or FHSA first?”

This is always goals-based. Short-, mid-, and long-term goals all matter. Income, pensions, and plans like buying a home all factor in. Most of the time, the answer isn’t one account, it’s a combination used intentionally.

“I save, but it doesn’t feel like it’s working. What am I missing?”

Usually it’s structure, not effort.

Expired savings promotions, high-cost investments, or being too conservative are common issues. Once the details are reviewed, this is often an easy fix.

“How much should I actually be investing each month?”

This is the number one question I get.

It requires understanding your income, expenses, current investments, age, and any pensions. Once those are clear, the path forward becomes obvious. A couple of hours spent here can mean the difference between retiring with $300,000 or $2 million.

“Do I need an advisor, or can I do this myself?”

This depends on personality.

How busy are you. How much detail do you want in your life. Do you enjoy managing this, or would you rather have a clear map and support. Neither option is right or wrong. It’s about what works for you.

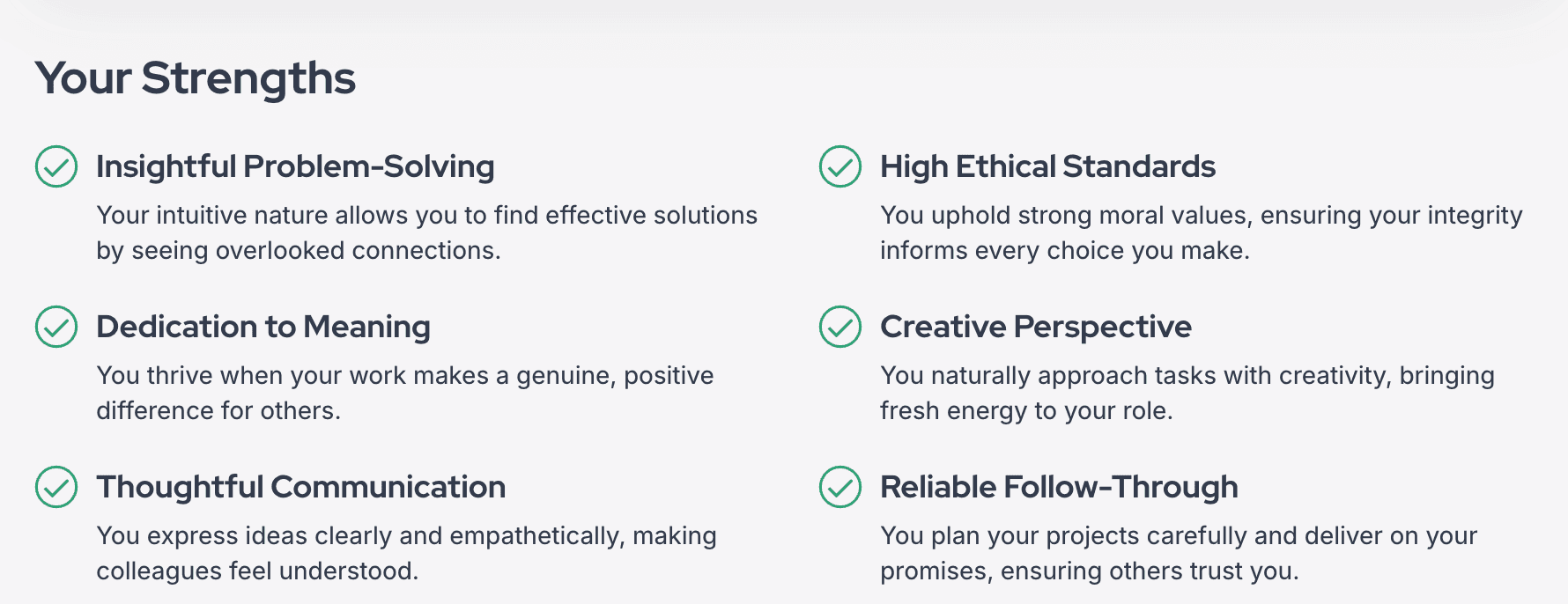

You can take a personality test here to learn more about your traits and how it may apply to different aspects of your life.

For those curious, I’m an INFJ. Many of those traits align naturally with the work I do as an advisor 😉:

There are many more questions I hear every week, but I’ll stop here.

I wanted to share these because the questions themselves matter. They tend to come from people who are paying attention and thinking ahead, not drifting or avoiding things.

If you recognized yourself in any of them, that’s usually not a sign something is wrong. It’s usually a sign you’re ready for clarity.

If you’ve been meaning to book an intro call and haven’t yet, the link is below. I’m always happy to chat and learn more about what you’re building.